A stablecoin is a type of cryptocurrency designed to hold a steady value by tracking a reference asset, most commonly the US dollar or the euro. Unlike Bitcoin or Ether, whose prices move freely with market demand, a stablecoin aims to trade at or very close to one unit of its reference at all times. The mechanism that holds the price steady varies: most stablecoins are backed 1:1 by cash and short-term government debt; others are over-collateralized with crypto-assets; a small category is backed by physical gold; and an older, now largely discredited category attempted to hold the peg using algorithms alone.

Stablecoins now move more value across blockchains than any other digital asset category and are increasingly integrated into regulated payment infrastructure, institutional trading venues, corporate treasury operations, and cross-border settlement networks, driven by expanding stablecoin use cases. Their combined market capitalization has crossed 300 billion US dollars and continues to grow as regulated frameworks like the EU's MiCA, the US GENIUS Act, the UK FCA regime, and Hong Kong's Stablecoin Ordinance bring banks, fintechs, and traditional financial institutions into the licensed-issuer perimeter.

This article explains exactly what a stablecoin is (a clear stablecoin definition), the four types of stablecoins, how each one maintains its peg, the major stablecoins in circulation today, the real risks behind them, what institutional compliance teams need to monitor, and how the global regulatory framework is reshaping the market.

A stablecoin is a cryptocurrency designed to maintain a stable value by being linked to an external reference such as the US dollar or the euro. It combines blockchain-native settlement with the price stability of fiat money.

A stablecoin is a crypto-asset issued on a blockchain that is designed to maintain a stable price relative to a reference asset. The reference can be a fiat currency (US dollar, euro, British pound), a basket of currencies, a commodity (gold being the most common), or, less commonly, another asset class entirely. The defining feature of a stablecoin is the stability mechanism. A stablecoin without a credible mechanism to hold its peg is just a poorly-pegged token. The mechanism falls into one of four categories, and the strength of that mechanism is what determines whether the stablecoin holds value through stress, depegs temporarily, or collapses entirely.

Stablecoins exist because the underlying problem they solve is real. Public blockchains move value globally, twenty-four hours a day, with final settlement in seconds. Bitcoin and Ether can move that value, but their prices change too quickly to function as a unit of account. A merchant cannot quote a price in Bitcoin if the value will shift several percent between order and settlement. Stablecoins close that gap: blockchain-native settlement with the price stability of fiat money.

If you're asking "how do stablecoins work", the answer centers on reserves, issuance and redemption mechanics, and market arbitrage that keeps the token near its reference value.

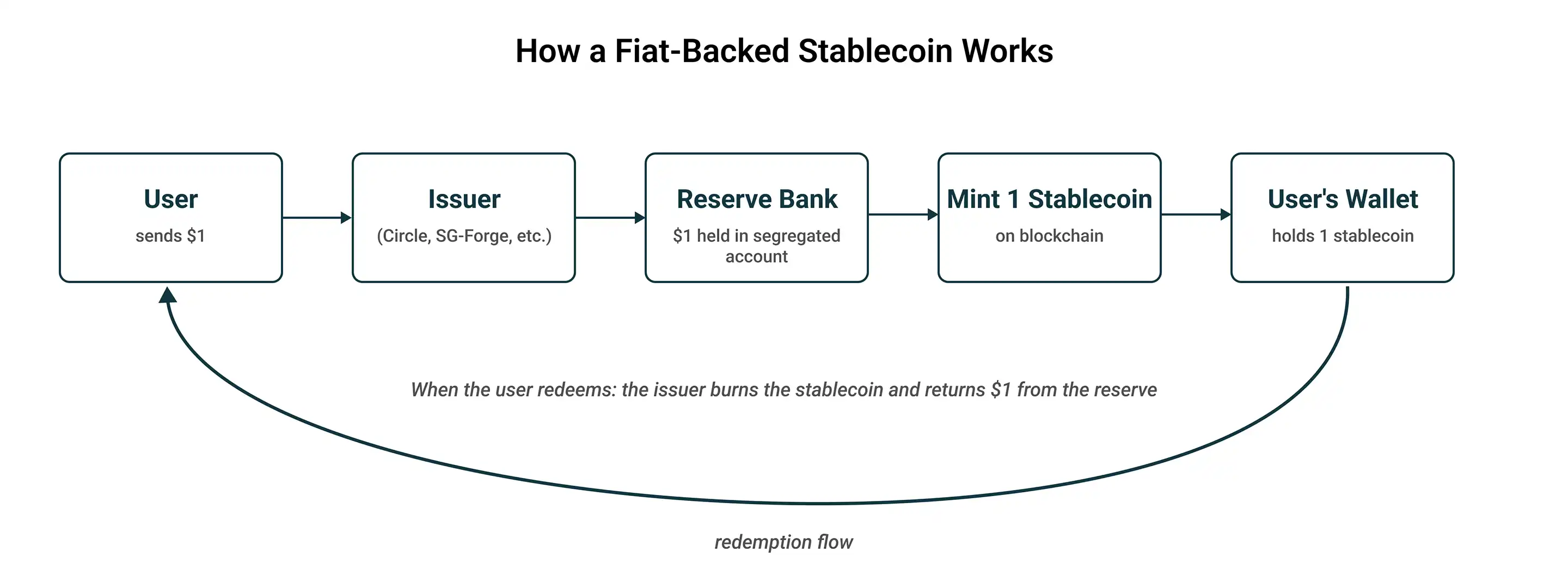

How does a stablecoin maintain its peg?

Most stablecoins maintain their peg by holding reserves equal to or greater than the circulating supply. When a user deposits fiat with the issuer, the issuer mints an equivalent stablecoin on-chain. When the user redeems, the stablecoin is burned and the fiat is returned. A stablecoin works by combining three components: a blockchain on which the token exists, an issuer (or a smart contract) that controls supply, and a stability mechanism that ties the token's market price to its reference asset.

The basic flow for a fiat-backed stablecoin works like this: a user sends one US dollar to the stablecoin issuer. The issuer adds that dollar to a reserve account at a regulated bank. The issuer then mints one new stablecoin and sends it to the user's blockchain wallet. The user can transfer, hold, or trade that stablecoin freely on-chain. When the user wants to redeem, the issuer burns the stablecoin and returns one dollar from the reserve.

Because every circulating stablecoin is matched by one dollar in reserve, the token trades at or near one dollar in secondary markets. If the price drifts above one dollar, arbitrageurs mint new stablecoins (paying one dollar to the issuer, selling on-chain for more), pushing the price back down. If it drifts below, they buy on-chain (below one dollar) and redeem with the issuer (for one dollar each), pushing the price back up.

Crypto-backed and commodity-backed stablecoins use a similar reserve principle but with different collateral. Algorithmic stablecoins try to skip the reserve step entirely, which is why most of them have failed.

The four types are fiat-backed (cash and government debt reserves), crypto-backed (over-collateralized with crypto-assets in smart contracts), commodity-backed (backed by physical commodities like gold), and algorithmic (supply controlled by algorithm, no full reserves).

Every stablecoin in circulation falls into one of four categories, defined by what backs the peg:

Fiat-backed stablecoins are the largest category by far and account for more than 95 percent of total stablecoin market value. Each token in circulation is matched 1:1 by cash, cash equivalents, and short-dated highly liquid government debt held in segregated accounts at regulated financial institutions. USDC, EURC, USDT, EURCV, and EURI all operate on this model.

Under MiCA, fiat-backed stablecoins fall into the e-money token (EMT) category, with specific obligations on reserve composition, segregation, redemption rights, and public attestation. In the EU, an authorized MiCA stablecoin (often informally written as "mica stablecoin") follows these EMT rules. Circle publishes weekly reserve attestations for USDC and EURC. Banking Circle and SG-Forge publish monthly. This transparency is what regulators require and what gives institutional treasuries the confidence to hold them at scale.

Crypto-backed stablecoins use other crypto-assets, locked in smart contracts, as collateral. Because crypto prices are volatile, the collateral is held at over 100 percent of the issued stablecoin value. A crypto-backed stablecoin such as DAI often requires roughly 150 percent collateralization: to mint 100 DAI, a user locks at least 150 dollars worth of Ether or other approved crypto-assets.

If the collateral price falls and the over-collateralization ratio breaches its minimum, the smart contract automatically liquidates the position to restore the peg. The mechanism is fully on-chain and removes the issuer as a single point of failure, but it introduces new risks: sudden collateral price crashes, smart contract vulnerabilities, and oracle failures.

Commodity-backed stablecoins are pegged to a physical commodity, almost always gold. Each token represents a claim on a specific amount of gold held in vaulted custody. PAXG and XAUT are the two largest examples, both tied to one troy ounce of physical gold per token. Under MiCA, commodity-backed stablecoins fall into the asset-referenced token (ART) category.

Algorithmic stablecoins attempted to maintain a peg using only algorithms, with no full reserve backing. The most famous example was TerraUSD (UST), which collapsed in May 2022 in a death spiral that wiped out 40 billion US dollars in value and triggered cascading failures across the crypto industry.

After 2022, algorithmic stablecoins are effectively prohibited under MiCA in the EU and treated as systemic risks by most other regulators. They survive only in unregulated corners of DeFi.

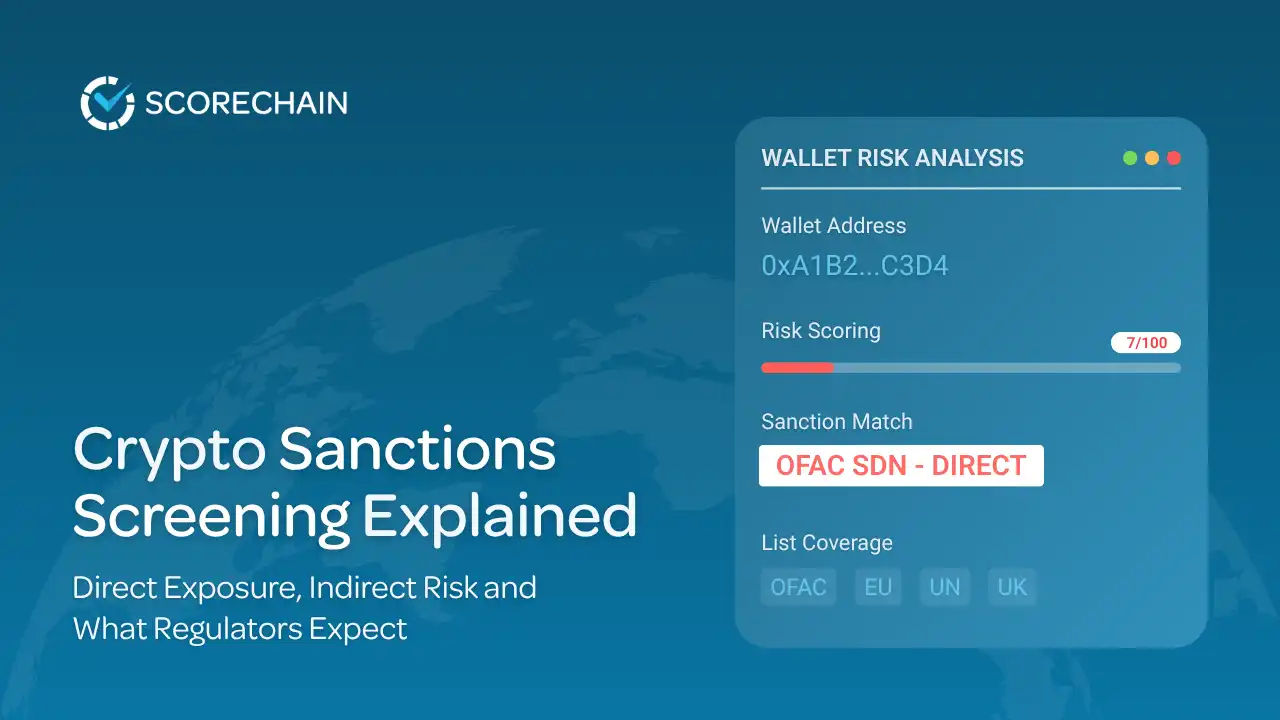

Stablecoins are designed to be stable, but they are not risk-free. The five main risks are: reserve quality, issuer solvency, regulatory action, de-pegging events under stress, and smart contract or operational failures. Stablecoins are designed to be stable, but they are not risk-free. Five risks deserve specific attention:

A fiat-backed stablecoin is only as strong as its reserves. If the reserves are held in low-quality assets, in unsegregated accounts, or with insufficient liquidity to honor redemptions during stress, the peg can break. The strongest stablecoins under MiCA and similar frameworks now hold reserves in cash deposits at regulated banks and short-dated government debt, audited regularly.

Even with sound reserves, a stablecoin holder depends on the issuer to honor redemptions. Issuer insolvency, regulatory enforcement actions, or operational failures can freeze redemptions. This is why MiCA requires authorized stablecoin issuers to be EU-regulated credit institutions or e-money institutions with capital adequacy requirements and ongoing supervision.

Regulatory action can affect stablecoins in two ways. First, an issuer may lose authorization or be barred from operating in a jurisdiction. Second, distribution platforms (exchanges, custodians) may be forced to delist a stablecoin even if the issuer continues operating elsewhere. The USDT delisting wave across EU exchanges in late 2024 and early 2025 is the clearest example: Tether did not lose its ability to operate globally, but it lost EU distribution because it did not seek MiCA authorization.

Even sound stablecoins can de-peg temporarily under stress. USDC briefly fell to 0.87 US dollars in March 2023 when Circle disclosed that 3.3 billion dollars of its reserves were held at Silicon Valley Bank, which had just failed. The peg restored within days once the US government confirmed depositor protection, but it demonstrated that even a high-quality stablecoin can wobble when its reserve venues are under stress.

For crypto-backed and algorithmic stablecoins, smart contract bugs, oracle manipulation, or governance attacks can cause the peg to break. For fiat-backed stablecoins on EVM chains, the issuer typically retains the ability to freeze and blacklist addresses, which provides a sanctions and law-enforcement compliance mechanism but introduces a centralization risk for holders.

Because stablecoin risk varies sharply by reserve composition, issuer status, and on-chain behavior, regulated institutions increasingly deploy continuous transaction monitoring and risk scoring across their stablecoin flows rather than relying on issuer attestations alone.

Six stablecoins account for the vast majority of circulating supply. Here is how they compare:

USDT remains the largest stablecoin globally by market capitalization, but its EU distribution has been cut off by MiCA. USDC has become the default compliant USD stablecoin in regulated markets. EURC, EURCV, EURI, and a growing list of smaller euro stablecoins serve EU on-chain payments. DAI continues to dominate decentralized stablecoin use cases, though its hybrid backing (now including a significant share of USDC in reserves) blurs the pure crypto-backed model.

Stablecoins started as a tool to move value in and out of crypto exchanges without the friction of bank wire transfers. They have since expanded into mainstream financial use cases:

For regulated institutions, the challenge with stablecoins is no longer understanding what they are. The challenge is understanding how they move, where they circulate, and what risks they may expose a business to.

Stablecoin activity now intersects directly with sanctions exposure, cross-border payment monitoring, illicit finance typologies, reserve transparency concerns, issuer concentration risk, and MiCA compliance obligations. Each of these moves what was once a custody question into the operational compliance perimeter.

Institutional teams now monitor:

As stablecoins become integrated into payment infrastructure and tokenized asset markets, transaction monitoring and risk scoring become operational requirements rather than optional controls.

Regulated CASPs running material stablecoin volume increasingly require real-time visibility into the on-chain behavior of every stablecoin flow passing through their venues, combined with audit-grade reporting that can withstand NCA review.

Where are stablecoins regulated?

Stablecoins are now regulated in four major jurisdictions: the European Union (under MiCA, from June 2024), the United States (GENIUS Act, July 2025), the United Kingdom (FCA regime under FSMA 2023), and Hong Kong (Stablecoin Ordinance, August 2025). All four require authorization, full reserve backing, and redemption rights.

The regulatory framework around stablecoins has matured dramatically across 2024, 2025, and 2026. Four jurisdictions now have comprehensive stablecoin regimes:

%20img.webp)

All four frameworks share the same architecture: authorization-gated issuance, full reserve backing, redemption rights, transparency obligations, and supervisory oversight. The convergence is significant because it sets up genuine cross-border interoperability for compliant stablecoins, while pushing non-compliant tokens to the margins of regulated finance.

For exchanges, custodians, banks, and fintechs operating across jurisdictions, MiCA-aligned monitoring infrastructure is now table stakes. The same standards (real-time risk scoring, sanctions screening, Travel Rule data integrity, audit-ready evidence trails) increasingly apply across the GENIUS Act, FCA, and Hong Kong regimes.

No. Bitcoin is a cryptocurrency whose price moves freely with market demand. Its value can change by several percent in a day, sometimes more, which is the opposite of a stablecoin's design. A stablecoin holds a steady value relative to a reference asset like the US dollar; Bitcoin holds no reference and is valued purely by what the market is willing to pay for it.

No. Ether (ETH), the native asset of the Ethereum blockchain, is a volatile cryptocurrency. Many stablecoins are issued on the Ethereum blockchain (USDC, USDT, DAI), but Ether itself is not a stablecoin.

No. XRP is a volatile cryptocurrency whose price changes with market demand. Ripple, the company associated with XRP, has separately issued RLUSD, which is a US-dollar stablecoin, but XRP and RLUSD are different assets.

The two most common classifications are by collateral type (fiat-backed, crypto-backed, commodity-backed, algorithmic) or by regulatory category under frameworks like MiCA (e-money tokens, which are pegged to a single currency, and asset-referenced tokens, which are pegged to a basket).

No. Stablecoins are designed to hold a stable value, but the strength of the peg depends on the quality of the backing, the credibility of the issuer, and the regulatory regime. Even high-quality stablecoins can de-peg temporarily during market stress. Algorithmic stablecoins have failed catastrophically. Investors should treat "stable" as an objective, not a guarantee.

In most regulated jurisdictions, you buy stablecoins on a licensed crypto exchange (Coinbase, Kraken, Bitstamp, and others) or directly from the issuer if they offer retail access. In the EU, after MiCA, only authorized stablecoins like USDC and EURC are available on regulated exchanges.

Yes, in major jurisdictions. The EU regulates stablecoins under MiCA, the US under the GENIUS Act, the UK under FCA rules, and Hong Kong under its Stablecoin Ordinance. Each framework requires authorization, full reserve backing, redemption rights, and supervisory oversight.

Stablecoins are crypto-assets engineered to hold a steady value. They work by tying the on-chain token to a real-world reference (most commonly the US dollar) through reserves, smart contract collateral, or algorithms. The four types behave differently under stress, and the regulatory frameworks that have emerged in the EU, US, UK, and Hong Kong are now defining which stablecoins can be offered to whom and under what conditions.

For institutional users, the question has shifted from whether stablecoins are a serious financial instrument (they clearly are) to which ones meet the regulatory and operational standards required to use them at scale. That question has clearer answers than ever before, and the gap between compliant and non-compliant stablecoins is widening fast.

Need to monitor stablecoin transactions for AML, Travel Rule, and MiCA compliance? Scorechain provides real-time risk scoring, sanctions screening, cross-chain visibility, and audit-grade reporting for stablecoin flows across all major blockchains. Talk to our team to see how Scorechain fits into your stablecoin compliance workflow.