Monday, May 11, 2026

Stablecoin regulation in the EU is now governed by a single, harmonized framework: the Markets in Crypto-Assets Regulation (MiCA), The Markets in Crypto-Assets Regulation (MiCA) introduces the first harmonized framework for crypto-assets across the European Union under the EU’s official regulatory framework published through EUR-Lex MiCA regulation. MiCA replaced a fragmented patchwork of national rules with a bloc-wide regime that defines exactly what a stablecoin is, who can issue one, how reserves must be held, and who can offer stablecoins to EU customers.

Stablecoin regulation in the EU is now governed by a single, harmonized framework: the Markets in Crypto-Assets Regulation (MiCA), formally Regulation (EU) 2023/1114. Introduced to unify crypto regulation across the European Union, MiCA defines how stablecoins can be issued, distributed, supervised and monitored within the bloc.

The result has reshaped the European stablecoin market in ways that are visible to anyone watching the major exchanges: Several EU-regulated exchanges have restricted or delisted USDT offerings for EEA users following MiCA implementation. Circle's USDC and EURC have emerged as leading MiCA-authorized stablecoins following Circle's regulatory approval process under the MiCA framework.

This article explains how stablecoin regulation works in the EU under MiCA: the two regulated stablecoin categories (e-money tokens and asset-referenced tokens), the authorization process for issuers, the obligations placed on crypto-asset service providers (CASPs) that distribute stablecoins, the implications of the July 1, 2026 transitional deadline, and how the EU framework relates to parallel regimes in the US, the UK, and Hong Kong.

Stablecoins in the EU are regulated under MiCA, which entered into force on June 29, 2023, and applies in stages. Stablecoin-specific provisions (Titles III and IV) became applicable on June 30, 2024. Provisions for crypto-asset service providers (Title V) applied from December 30, 2024. The regulation creates two regulatory categories for stablecoins, defines specific authorization pathways for issuers, and prohibits the public offering or trading of any stablecoin that is not authorized under one of those categories.

MiCA's design has three structural consequences for the EU stablecoin market:

Under MiCA, every regulated stablecoin falls into one of two categories: e-money tokens (EMTs) or asset-referenced tokens (ARTs). The distinction matters because reserve rules, redemption mechanics, and supervisory oversight change significantly between them.

In practice, the EMT category dominates. Every stablecoin authorized under MiCA to date (USDC, EURC, EURI, EURCV, EURe, EURD, EUROe) is an e-money token. No asset-referenced token has been authorized, reflecting the higher capital and prudential requirements ARTs face under Title III and limited market demand for multi-asset-backed stablecoins compared to single-currency pegs.

MiCA authorization is not a one-time filing. It is a continuous obligation built around five operational pillars:

The list of MiCA-authorized stablecoins has expanded steadily since 2024. The publicly authorized e-money tokens include:

ESMA's public register is the authoritative source and is updated continuously as NCAs grant new authorizations. Additional EMTs that have entered the register from regional EU issuers include EURØP, EURR, USDR, USD1, eUSD, EURQ, USDQ, and ENEUR, expanding the multi-currency stablecoin landscape.

Tether's USDT is the largest stablecoin globally by market capitalization, but it has not pursued MiCA authorization. The mechanism that drove its removal from EU venues is structural rather than punitive:

The delisting wave ran from late 2024 through Q1 2025. Coinbase Europe announced removal of non-compliant stablecoins in early December 2024. Crypto.com followed in January 2025. Binance delisted USDT spot pairs for EEA users on March 31, 2025. Kraken moved USDT to sell-only mode in late March 2025. OKX and Bitstamp implemented similar restrictions for their EU customer segments.

EU users can still hold USDT in self-custody wallets, transact on decentralized exchanges, and use it in DeFi protocols. Those activities sit outside MiCA Title V's perimeter. What they cannot do is buy, sell, or hold USDT through a MiCA-authorized centralized service provider.

July 1, 2026 marks the end of MiCA's EU-wide transitional period for crypto-asset service providers. After that date, any entity providing crypto-asset services in the EU without full MiCA authorization is in breach of EU law and must cease offering those services to EU customers. ESMA has been explicit on this point.

Member states adopted different transitional windows under the regulation's grandfathering provisions:

For stablecoin issuers and the CASPs that distribute them, the practical implication is that EU stablecoin compliance is no longer a future consideration. It is the operating reality. Every listing decision, custody arrangement, and treasury allocation involving stablecoins must map cleanly to authorization status and supervisory expectations.

A bank onboarding a crypto-native corporate client may now need to assess whether incoming stablecoin exposure involves MiCA-authorized EMTs or non-authorized instruments routed through offshore venues. This moves stablecoin assessment beyond listing status and into operational risk, counterparty exposure and ongoing transaction monitoring.

MiCA is no longer a regional outlier. A converging global framework for stablecoin regulation has taken shape across 2025 and 2026:

All three regimes share MiCA's core architecture: authorization-gated issuance, full reserve backing, redemption rights, and supervisory oversight. The differences lie in scope, prudential thresholds, and how each treats algorithmic and yield-bearing structures. For multinational treasury teams and exchanges, MiCA increasingly functions as the de facto reference framework against which other jurisdictions are calibrated.

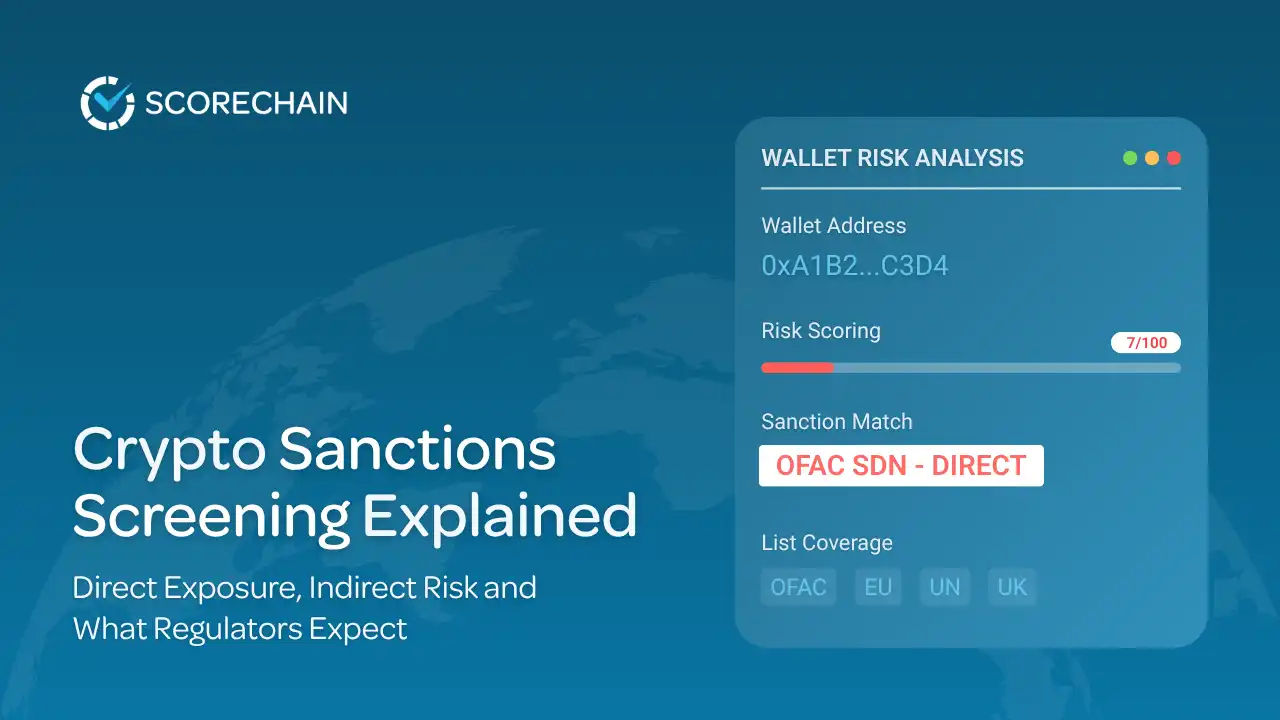

For CASPs, banks, payment firms and stablecoin issuers, MiCA compliance is not limited to checking whether a token appears on an authorized list. It affects listing decisions, transaction monitoring, Travel Rule processes, sanctions screening, counterparty reviews and audit evidence.

Three operational shifts deserve direct attention.

Stablecoin orchestration platforms, payment rails, and exchange listing engines must encode MiCA authorization as a first-class routing variable. A settlement route ending in USDC for an EU customer is MiCA-compliant. The same route ending in USDT is not, regardless of chain or transport rail. Real-time compliance checks at the transaction level, rather than periodic policy updates, are the new baseline.

MiCA does not exist in isolation. It operates alongside AMLD6, the EU Transfer of Funds Regulation, and the FATF Travel Rule. Every stablecoin flow through an EU-licensed CASP must be screened for sanctions exposure, high-risk counterparty contact, mixer or obfuscation patterns, and Travel Rule data sufficiency. For high-throughput stablecoin volumes, this is not feasible without dedicated blockchain analytics infrastructure.

MiCA-licensed entities face annual NCA reviews and incident-driven examinations. Maintaining a defensible record of every alert, screening decision, suspicious activity report, and remediation action across stablecoin flows specifically has shifted from a nice-to-have to a regulatory expectation.

This is precisely the operational layer Scorechain is built for. Real-time risk scoring across major chains, automated Travel Rule compliance, sanctions and KYC screening tuned to EU requirements, and audit-grade reporting aligned with BaFin, ACPR, CSSF, and CNMV expectations all sit within a single MiCA-aligned compliance workflow. CASPs and stablecoin issuers preparing for the July 2026 deadline (or already operating under MiCA authorization) use Scorechain to make stablecoin compliance both auditable and operationally seamless.

MiCA compliance increasingly requires institutions to understand not only whether a stablecoin is authorized, but also how it is distributed, held and exposed to risk across the market.

Scorechain’s Digital Asset Intelligence provides asset-level visibility into stablecoins and tokenized assets, including holder concentration, mint and burn activity, transaction flows, exposure to sanctioned entities and abnormal on-chain behaviour.

This allows CASPs, banks, fintechs and stablecoin issuers to assess circulating supply dynamics, monitor reserve-related activity and identify operational or compliance risks linked to stablecoin usage across multiple blockchains.

Under MiCA, stablecoin compliance is becoming an operational monitoring challenge rather than a static policy exercise.

Institutions need visibility into stablecoin transaction flows, sanctions exposure, high-risk counterparties, mixer interaction and Travel Rule obligations across multiple chains and customer environments.

Scorechain enables real-time stablecoin monitoring with configurable risk scoring, automated transaction screening, audit-ready reporting and blockchain analytics aligned with European supervisory expectations.

Stablecoins in the EU are regulated under the Markets in Crypto-Assets Regulation (MiCA), formally Regulation (EU) 2023/1114. Stablecoin-specific provisions applied from June 30, 2024, and provisions for crypto-asset service providers applied from December 30, 2024.

Yes. Circle's USDC is authorized as an e-money token under MiCA, issued through Circle's EU-authorized entity (Circle SAS, France). It is the largest MiCA-compliant USD-pegged stablecoin and is offered on EU-regulated exchanges across the bloc.

No. Tether has not applied for MiCA authorization. USDT has been delisted from major EU-regulated exchanges including Coinbase, Kraken, Binance (EEA), and Crypto.com. It can still be held in self-custody and traded on decentralized exchanges, but cannot be offered by EU-licensed CASPs.

An EMT is pegged to a single official currency and issued by an authorized EMI or credit institution under MiCA Title IV. An ART is backed by a basket of assets (multiple currencies, commodities, or other instruments) and falls under Title III with stricter prudential requirements. Every authorized MiCA stablecoin to date is an EMT.

No. Algorithmic stablecoins without tangible reserve backing are effectively prohibited. MiCA requires every authorized stablecoin to be fully backed 1:1 by liquid reserves held in segregated accounts.

No. MiCA explicitly prohibits issuers from granting interest on EMTs and ARTs, regardless of how the yield is structured.

The EU-wide transitional period for crypto-asset service providers ends on July 1, 2026. Some member states adopted shorter windows, including Germany, Austria, and Ireland (late 2025) and the Netherlands and Poland (mid-2025).

EU stablecoin regulation under MiCA has shifted the European market from a question of whether to comply to a question of how. The authorized issuer list is short but growing. The non-compliant tail is being squeezed out of regulated distribution. And the framework is increasingly being mirrored, through the GENIUS Act, FCA rules, and Hong Kong's Stablecoin Ordinance, across the jurisdictions that matter for global crypto infrastructure.

For exchanges, custodians, banks, fintechs, and stablecoin issuers operating in or serving the EU, the compliance question has narrowed to something concrete: can your stablecoin distribution, monitoring, and audit infrastructure withstand an NCA review tomorrow? If the answer is anything less than "yes, demonstrably," the time to close the gap is now.

Ready to operationalize EU stablecoin compliance? Scorechain helps CASPs, exchanges, and stablecoin issuers across the EU automate AML monitoring, Travel Rule compliance, sanctions screening, and audit-ready reporting, all aligned with MiCA's supervisory expectations. [Talk to our compliance team] to see how Scorechain fits into your MiCA roadmap.