Quick overview

Every blockchain transaction creates a permanent, immutable record. KYT platforms continuously collect and analyse this data across supported networks, creating real-time visibility into the movement of digital assets between wallet addresses. This forms the foundation of all subsequent risk assessments. Know Your Transaction (KYT) is theprocess of monitoring, analyzing, and assessing cryptocurrency transactions toidentify financial crime risks, sanctions exposure, suspicious activity, andcompliance concerns.

Unlike Know Your Customer (KYC), which focuses on verifying customer identities during onboarding, KYT focuses on understanding how digital assets move across blockchain networks and whether those transactions create regulatory or risk management concerns.

KYT has become a critical componentof modern crypto compliance programs. Banks, Crypto-Asset Service Providers(CASPs), exchanges, custodians, payment providers, and fintech companies use KYT to strengthen Anti-Money Laundering (AML) controls, detect suspicious activity, investigate high-risk transactions, and meet obligations across multiple regulatory jurisdictions.

Why KYT matters in crypto compliance

The rapid growth of digital assets has created significant opportunities for financial institutions. Banks are exploring crypto custody services. Payment providers are supporting digital asset transfers. Institutional investors are increasing their exposure to digital assets. CASPs are expanding operations across multiple jurisdictions.

At the same time, regulators across Europe, the United States, the United Kingdom, the Middle East, and Asia-Pacific have intensified their focus on financial crime risks within the digital asset ecosystem. Unlike traditional banking systems, blockchain transactions can cross borders instantly, interact with decentralised services, and involve counterparties operating under entirely different regulatoryframeworks.

A customer may successfully passonboarding checks, provide legitimate identification, and appear low riskduring account opening. However, weeks or months later, that same customer could receive funds from a wallet associated with sanctions violations, ransomware groups, darknet marketplaces, fraud schemes, or other forms of illicit activity. Identity verification alone cannot identify these risks.

Expert insight

Most compliance failures in crypto do not happen atonboarding. They happen afterwards. A customer who passes every KYC check onday one can receive funds from a sanctioned entity on day 90. The compliance gap is not in who you onboard. It is in what you monitor once they are active. KYT exists to close that gap, and regulators in every major jurisdiction are now examining whether firms have done so.

The evolution of crypto compliance

In traditional finance, compliance frameworks typically rely on customer due diligence and transaction monitoringwithin closed, regulated financial networks. The crypto ecosystem operates differently. Funds can move between centralised exchanges, decentralised protocols, self-hosted wallets, custodians, payment services, and cross-chain bridges in minutes, across jurisdictions that may have no regulatory relationship with each other.

This requires additional layers of visibility that traditional compliance tooling was not designed to provide.

KYT does not replace traditional compliance controls. It extends them to address the unique characteristics of blockchain-based transactions, providing the additional layer of intelligence that regulators across every major jurisdiction now expect financial institutions to demonstrate.

What risks is KYT designed to identify?

Effective KYT programs help organisations identify a broad range of financial crime and compliance risks. The scope extends well beyond money laundering.

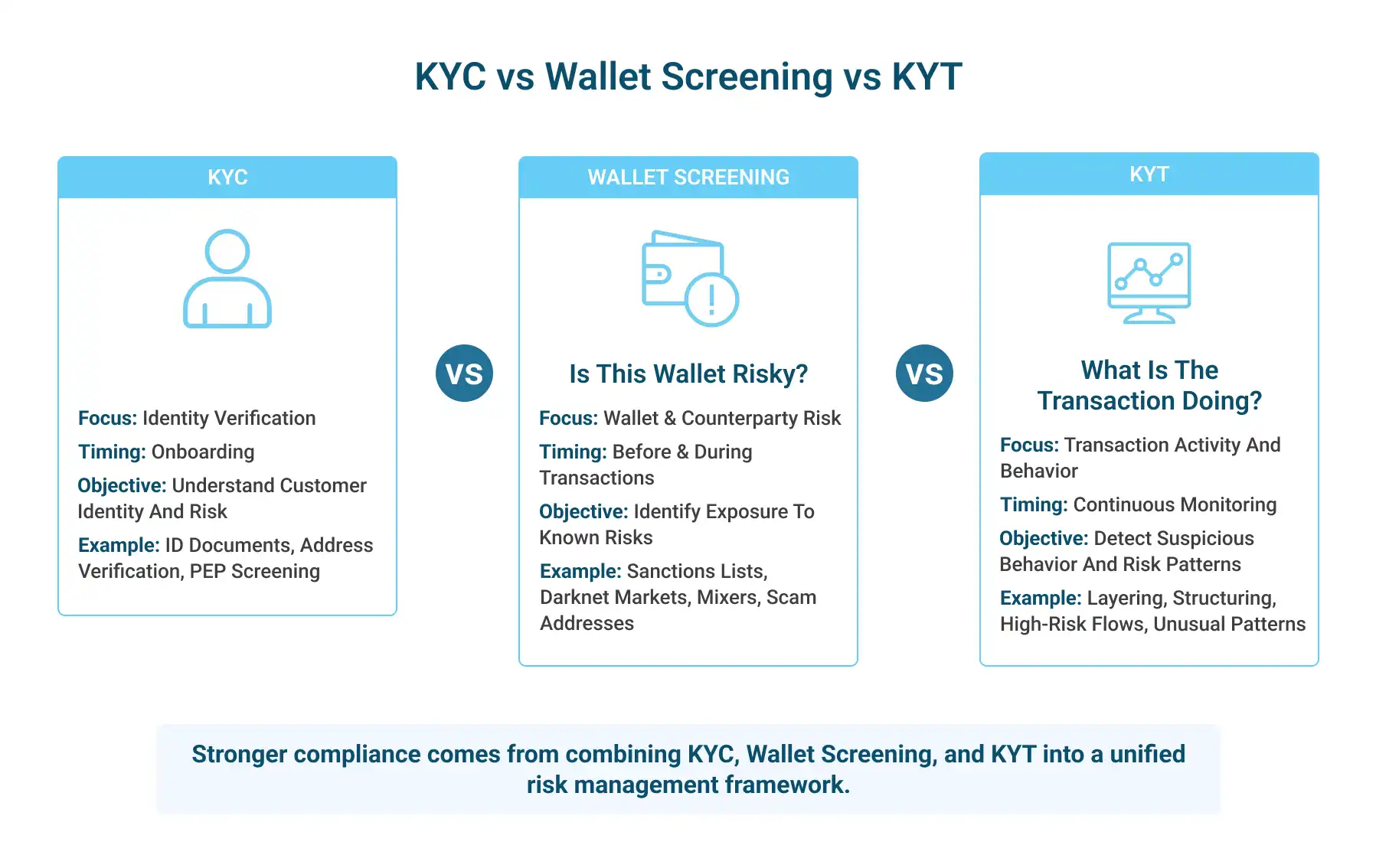

KYT vs KYC vs wallet screening

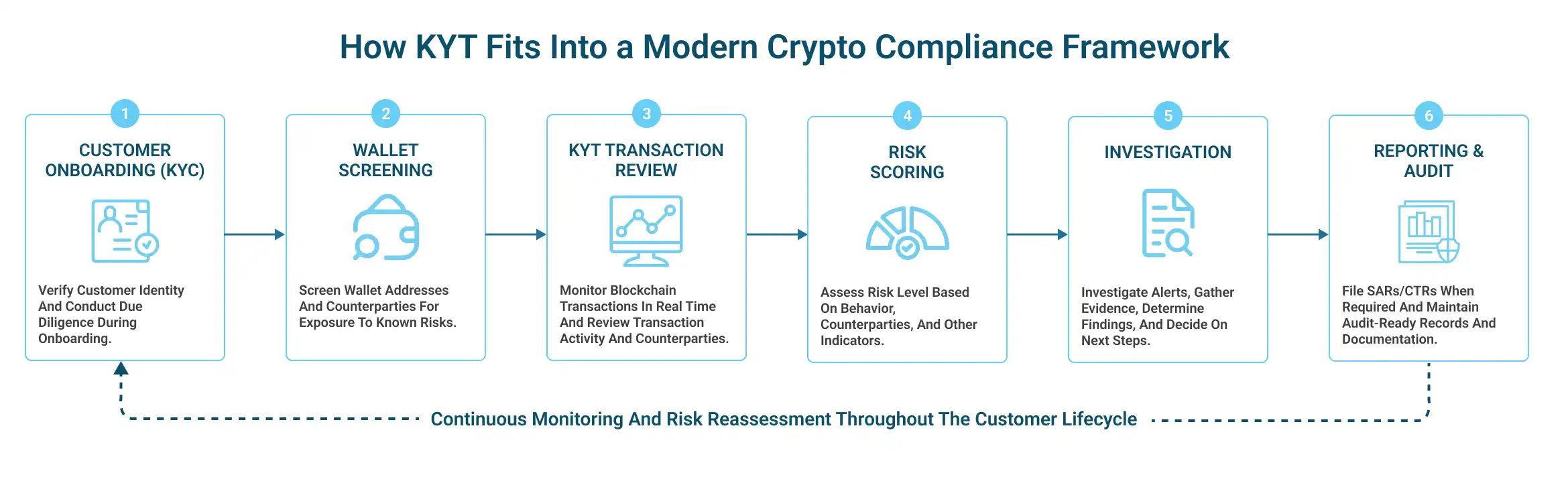

How KYT works in practice

Although implementation varies between organisations, most KYT programs follow a similar process. The objective is to transform raw blockchain transaction data into actionable compliance intelligence.

1) Monitoring blockchain activity

Every blockchain transaction creates a permanent, immutable record. KYT platforms continuously collect and analyse this dataacross supported networks, creating real-time visibility into the movement of digital assets between wallet addresses. This forms the foundation of all subsequent risk assessments.

2) Wallet attribution and entity identification

Raw blockchain data provides limited insight on itsown. A wallet address is a string of characters without context. KYT solutions enrich transaction data by identifying known entities associated with walletaddresses, including exchanges, custodians, payment providers, decentralised protocols, darknet services, mixer services, and sanctioned entities. Thiscontext helps compliance teams understand who may be involved in a transaction, not just where funds moved.

3) Risk assessment and scoring

Once transaction context has been established, risk indicators are evaluated. Transactions may be assessed based on exposure tosanctions, suspicious counterparties, unusual behavioural patterns, high-risk jurisdictions, indirect hop-depth connections, or other indicators defined within an organisation's compliance framework. The objective is to prioritiseactivity that warrants further review, not to flag every transaction.

4) Alert generation and investigation

When predefined risk thresholds are exceeded, alerts are generated for compliance review. Investigators can assess the activity, review entity attribution and transaction path evidence, document findings, and determine whether escalation, enhanced due diligence, or regulatory reporting is required. Structured investigation workflows improve consistency and auditreadiness.

The three pillars of effective KYT

Many organisations approach KYT as a technology procurement decision. In practice, the most effective compliance programs recognise that transaction monitoring requires three capabilities working together.

1) Visibility

Organisations cannot manage risks they cannotsee. The first objective of any KYT program is to provide genuine visibility into the movement of digital assets across blockchain networks. Compliance teams need to understand where funds originate, where they are sent, whichentities are involved, and how assets move across the broader ecosystemincluding cross-chain bridges, mixing services, and decentralised protocols. Without visibility, compliance is reactive by definition.

2) Risk intelligence

Visibility alone is not sufficient. Modern blockchain networks generate enormous volumes of transaction data. The challenge is not obtaining data but understanding what it means. A transaction involving a newly created wallet may appear benign. Additional analysis may reveal indirect exposure to a sanctioned entity four hops away, or a behavioural pattern consistent with layering across 11 wallets on three different networks. Risk intelligence is what separates raw data from actionable compliance insight.

3) Investigation readiness

Alert generation is the easiest part of KYT. Investigation is where compliance programs succeed or fail. An effective KYT program ensures that when an alert fires, the compliance team can immediately understand why it fired, which specific risk indicators were identified, how severe the risk may be, and what evidence supports the decision. Regulators examining KYT programs do not simply look for alert counts. They look for documented, reasoned decisions.

KYT in practice: four scenarios

The following scenarios illustrate how Scorechain's KYT capabilities identify compliance risks across different customer types and risk categories. All situations are illustrative. Statistics are verified Scorechain platform figures.

The KYT maturity model

Not all KYT programs are equallyeffective. Organisations tend to progress through three stages of maturity astheir digital asset compliance capabilities develop.

Level 1: Reactive monitoring

• Spreadsheet-based reviews and manual blockchain investigations

• Limitedor single-chain visibility with no cross-chain tracing

• Reactive, point-in-time checks rather than continuous monitoring

• High operational workload with inconsistent documentation

• Alert volume ungoverned and alert quality unmeasured

Level 2: Risk-based monitoring

• Automated alerts based on predefined risk thresholds

• Wallet screening integrated into transaction workflows

• Risk scoring and prioritisation reducing investigator workload

• Defined escalation procedures and structured case management

• Consistent documentation supporting audit readinessand SAR filing

Level 3: Intelligence-driven compliance

• Continuous monitoring across all supported networks with hop-depth analysis

• Advanced risk intelligence integrated into enterprise risk management strategy

• Automated case management with cross-functional collaboration

• Audit-ready documentation and data-driven decision making

• KYT outputs used to inform customer risk ratings and refresh due diligence cycles

Expert insight

The most revealing question to ask about any KYT program is not how many alerts it generates. It is how many of those alerts result in documented decisions. Regulators examining program effectiveness want to see evidence that alerts were reviewed, assessed, and resolved with a clear rationale. Alert volume without investigation quality is not a compliance program. It is a liability.

KYT vs KYC vs Wallet Screening

One of the most common areas ofconfusion in crypto compliance is the relationship between KYC, KYT, and wallet screening. These controls address different objectives and operate at different points in the customer lifecycle.

These controls are complementary, not interchangeable. KYC establishes confidence in customer identity. Wallet screening identifies potential exposure at the address level. KYT monitors how assets move after onboarding begins. The strongest compliance frameworks integrate all three into a unified risk management process that operates throughout the entire customer lifecycle.

Common misconceptions about KYT

Misconception 1: KYC is sufficient

Customer onboarding checks cannot identify risks that emerge from post-onboarding transaction behaviour. A customer who receives funds from a ransomware wallet three months after passing all KYC checks presents areal compliance failure that KYC alone has no mechanism to detect. Regulators in every major jurisdiction have made clear that ongoing monitoring is aseparate and distinct obligation from identity verification.

Misconception 2: KYT is only for crypto exchanges

Exchanges were early adopters, but KYT is now operationally necessary for banks offering crypto custody, payment providers processing digital assets, asset managers holding digital portfolios, fintech companies integrating blockchain payment rails, and any CASP operating under MiCA, FCA, FinCEN, VARA, or MAS frameworks.

Misconception 3: High-risk alerts mean suspicious activity

Exchanges were early adopters, but KYT is now operationally necessary for banks offering crypto custody, payment providers processing digital assets, asset managers holding digital portfolios, fintech companies integrating blockchain payment rails, and any CASP operating under MiCA, FCA, FinCEN, VARA, or MAS frameworks.

Misconception 4: KYT is a one-time configuration

Financial crime typologies evolve continuously. Monitoring rules, risk thresholds, and entity databases that were effective 12 months ago may not adequately address current threats including new mixer protocols, emerging darknet markets, cross-chain bridging techniques, or newly designated sanctions targets. Effective KYT programs require regular review and calibration.

Misconception 5: Manual processes scale

At low transaction volumes, manual blockchain review is possible. It is not sustainable. Organisations that rely on spreadsheets and ad hoc blockchain explorer searches will face a compliance capacity crisis as volumes grow, and regulators examining their programs willfind the evidence trail inconsistent and incomplete.

KYT for banks

Banks entering the digital assetecosystem face a compliance challenge that is qualitatively different from whatcrypto-native firms encounter. Banks operate within mature governance frameworks,are subject to supervisory examination by central banks and prudential regulators, and carry reputational exposure that a compliance failure indigital assets can damage across their entire business.

Regulators applying supervisory scrutiny to banks' digital asset programs examine not just whether policies exist, but whether controls are effective in practice. The European BankingAuthority (EBA) has issued guidance making clear that AML obligations apply fully to banks' crypto-related activities. The Financial Conduct Authority(FCA) in the United Kingdom expects registered crypto firms, including bank subsidiaries, to demonstrate transaction monitoring programs proportionate to their risk exposure. The Office of the Comptroller of the Currency (OCC) in theUnited States has addressed the conditions under which banks may engage in digital asset activities, with AML controls as a prerequisite.

What bank supervisors look for in a KYT program

• Continuous transaction monitoring, not periodic sampling

• Documented risk-based thresholds with evidence of calibration reviews

• Structured investigation workflows producing defensible compliance decisions

• Alert quality metrics, not just alert volume

• Integration between KYT outputs and customer risk rating refresh processes

• Evidence that high-risk alerts resulted in reviewed, documented, and resolved cases

• Audit-ready records capable of supporting regulatoryexamination and SAR filing

Expert insight

Banks are not penalised by supervisors for identifying suspicious activity. They are penalised for failing to identify it, or for identifying it and failing to act on it in a documented and timely way. A KYT program that generates alerts but lacks investigation depth is more likely to create regulatory exposure than one that generates fewer, higher-quality alerts with complete investigation records.

KYT for CASPs

Crypto-Asset Service Providers operate at the centre of the digital asset ecosystem. Their customers interact with exchanges, self-hosted wallets, decentralised protocols, custodians, andpayment networks simultaneously. This creates a more dynamic and complex riskenvironment than most traditional financial institutions face.

Under the Markets in Crypto-AssetsRegulation (MiCA), CASPs authorised within the European Union must demonstraterobust governance, risk management, and AML compliance. The Travel Rule, asimplemented across jurisdictions including the EU, UK, Switzerland, Singapore,and the UAE, also requires CASPs to collect and transmit originator andbeneficiary information alongside digital asset transfers, making transaction data quality foundational to compliance.

KYT helps CASPs monitor customeractivity at scale, detect behavioural anomalies, identify emerging threats innear real time, support AML and Travel Rule obligations, and improve theoperational efficiency of compliance teams managing large transaction volumes.

KYT in global regulatory frameworks

KYT obligations exist across every major financial jurisdiction. While the terminology and specific requirements differ, the underlying expectation is consistent: organisations handling digital assets must monitor transactions on an ongoing basis, assess risk incontext, and generate documented compliance decisions.

The Financial Action Task Force(FATF) provides the global foundation. FATF Recommendation 15 requires member jurisdictions to regulate Virtual Asset Service Providers for AML and counter-terrorism financing purposes, including transaction monitoring. The2021 FATF Updated Guidance on Virtual Assets sets out detailed expectations for how monitoring should operate in blockchain environments, including the need toassess indirect exposure through multi-hop analysis. Every domestic frame worklisted below is built on this foundation.

Each jurisdiction translates theseobligations differently. The EU and UK have the most prescriptive implementation frameworks currently in force. The US applies existing BSA obligationsto virtual currency businesses through FinCEN guidance and enforcementprecedent. The UAE and Singapore have built purpose-built regulatory frameworkswith explicit rulebooks for each licensed activity type. Switzerland and Japanhave the longest track records of virtual asset AML enforcement among non-EUjurisdictions.

Dedicated compliance guides foreach jurisdiction are available in the Scorechain resource library. Theremainder of this section focuses on MiCA, the framework most directly relevantto Scorechain's European client base and one of the most structurallysignificant developments in crypto regulation globally.

KYT and MiCA compliance

The Markets in Crypto-AssetsRegulation (MiCA) represents the most comprehensive crypto-specific regulatory framework currently in force globally. While MiCA does not use the term 'KYT' explicitly, it creates specific obligations that make transaction monitoringoperationally necessary for all CASPs authorised within the European Union.

MiCA requires CASPs to establishand maintain governance arrangements, risk management frameworks, and AML controls proportionate to the nature, scale, and complexity of theiractivities. The Transfer of Funds Regulation, which applies in parallel, removes the EUR 1,000 de minimis threshold for crypto asset transfers, meaningevery transaction must be accompanied by originator and beneficiary data, andevery transaction is subject to monitoring obligations.

How KYT strengthens AML programs

KYT should be understood as one component within a broader Anti-Money Laundering framework, not as a standalone solution. A mature AML program includes Customer Due Diligence (CDD), Enhanced Due Diligence (EDD), risk assessments, transaction monitoring, investigations,and regulatory reporting. KYT strengthens each of these components by providingdeeper visibility into blockchain-based financial activity.

Customer due diligence mayestablish expected transaction behaviour during onboarding. KYT determines whetheractual activity aligns with those expectations over time. Where it does not,KYT provides the documented evidence trail that supports an enhanced duediligence review, a risk rating refresh, or a SAR filing. The two processes arenot alternatives. They are complementary stages of a continuous compliancelifecycle.

Common challenges when implementing KYT

While the case for KYT is clear, implementation presents operational and technical challenges that organisationsshould anticipate.

Alertfatigue and false positive rates

Poorly configured monitoring rulescan generate large volumes of alerts that prove to be low risk on investigation. This overwhelms compliance teams, increases response times, andreduces the overall quality of compliance decision making. Effective KYT programs focus on improving alert precision through better risk intelligenceand regular threshold calibration, not simply maximising alert volume.

Cross-chaincomplexity

Digital assets increasingly move across multiple blockchain networks via bridges and interoperability protocols. A transaction that originates on Ethereum may involve assets that have passed through Polygon, Avalanche, or Solana. Understanding the full risk picture requires visibility across all relevant networks, not just the chain on which the final transaction appears.

Evolvingfinancial crime typologies

Criminal actors adapt continuously. Techniques that effective monitoring would have caught 18 months ago may now be routed differently, use new mixing protocols, or exploit newlylaunched cross-chain infrastructure. Monitoring rules and entity databases must be updated regularly to remain effective against current threats.

Resourceand capacity constraints

Many compliance teams face growingtransaction volumes without proportional growth in headcount. Technologyimproves efficiency and consistency, but experienced compliance professionalsremain essential for investigation quality and defensible decision making.Organisations should plan for the human capacity requirements of a mature KYTprogram, not just the technology procurement.

Multi-jurisdictioncompliance harmonisation

Organisations operating acrossmultiple jurisdictions face the challenge of meeting overlapping regulatoryrequirements that may have different thresholds, reporting timelines, anddocumentation standards. A KYT program designed for MiCA may need adjustment toalso satisfy FCA, FinCEN, VARA, and MAS expectations simultaneously.

Best practices for effective KYTprograms

1) Adopt a risk-based approach

Not all transactions carry the same level of risk. Compliance resources should be concentrated where they have the greatest impact. Risk-based approaches, as required by FATF, MiCA, FCA, FinCEN, VARA,and MAS alike, mean calibrating monitoring rules to the actual risk profile ofthe business, its customers, and its transaction types rather than applying uniform thresholds to all activity.

2) Integrate KYC, wallet screening, and KYT

No single control provides complete protection. KYCestablishes identity confidence at onboarding. Wallet screening assesses address-level exposure before and during transactions. KYT monitors behavioural patterns across the full transaction lifecycle. The three controls together create a compliance framework that addresses risks at every stage of thecustomer relationship.

3) Monitor continuously, not periodically

Risk does not respect review schedules. A sanctions designation can be issued on any day of the year. A customer can receive fundsfrom a ransomware wallet on a bank holiday. Continuous monitoring ensures that risks are identified as close to the point of exposure as possible, enabling intervention before assets move on and the compliance window closes.

4) Build investigation depth, not just alert breadth

Regulators examining KYT programs are not primarily interested in alert counts. They want to see that alerts are reviewed promptly,that the review process is documented, that decisions are supported byevidence, and that suspicious activity results in appropriate escalation orreporting. Alert generation without investigation infrastructure is acompliance gap, not a compliance program.

5) Review and calibrate monitoring rules regularly

The crypto ecosystem evolves faster than mostcompliance programs are updated. Monitoring rules that were effective againstlast year's typologies may be inadequate today. Organisations should schedule regular reviews of risk thresholds, entity databases, and detection logic, and should document those reviews as evidence of a living compliance program.

6) Design for multi-jurisdiction compliance from the start

Organisations with customers or operations across multiple jurisdictions should design their KYT programs to satisfy the most demanding applicable framework as a baseline. Building a program to MiCA and FCA standards simultaneously will generally produce a program that also satisfies FATF baseline expectations for other jurisdictions.

Industry trends shaping KYT

Frequently asked questions

Is KYT required under MiCA?

MiCA does not use the term 'KYT' explicitly, but it requires CASPs to implement governance, risk management, and AML controls that make transaction monitoring operationally necessary. The Transfer of Funds Regulation, which applies in parallel, mandates ongoing monitoring of allcrypto asset transfers with no de minimis threshold.

What is FATF Recommendation 15 and how does it relate to KYT?

FATF Recommendation 15 requires member jurisdictions to ensure that Virtual Asset Service Providers are regulated for AML and counter-terrorism financing purposes, including transaction monitoring. The 2021 FATF Updated Guidance on Virtual Assets provides detailed expectations for blockchain monitoring, including risk-based approaches to indirect exposure assessment.This guidance underpins the domestic frameworks of all member jurisdictions, from the EU and UK to the US, UAE, Singapore, Switzerland, Hong Kong, andJapan.

Is KYT required in other jurisdictions beyond the EU?

Yes. Transaction monitoring obligations apply across all major financial jurisdictions. The FCA requires it for UK-registered cryptoassetbusinesses under the Money Laundering Regulations 2017. FinCEN requires it forUS virtual currency MSBs under the Bank Secrecy Act. VARA requires it for UAE-licensed VASPs. MAS requires it for Singapore DPT service providers. FINMA requires it for Swiss financial intermediaries. The SFC requires it for HongKong VATPs. The FSA requires it for Japanese crypto-asset exchange serviceproviders. The regulatory table in this article maps each jurisdiction's primary framework and obligation level.

Does KYT replace KYC?

No. KYC and KYT address different risks at different points inthe customer lifecycle. KYC focuses on identity verification during onboarding. KYT focuses on transaction behaviour throughout the ongoing customer relationship. Both are required by all major regulatory frameworks.

What triggers a KYT alert?

Alerts may be triggered by direct or indirect exposure to sanctions-listed entities, transactions involving high-risk wallet clusters, behavioural deviations from established customer profiles, interactions withdarknet services or mixing protocols, unusual transaction volumes or patterns, or other predefined risk indicators calibrated to the organisation's riskappetite.

Can KYT detect indirect sanctions exposure?

Yes. Hop-depth analysis is a core capability of advanced KYT programs. Exposure to a sanctioned entity that sits three or four hops from the direct counterparty may be invisible to manual review but detectable through automated multi-hop tracing. OFAC has taken enforcement action in casesinvolving indirect exposure.

Can banks use KYT?

Yes, and they increasingly must. Banks offering crypto custody, stablecoin payment services, or digital asset trading are expected by the EBA,FCA, OCC, and other prudential regulators to demonstrate transaction monitoring capabilities proportionate to their risk exposure.

What is the difference between KYT and blockchain analytics?

Blockchain analytics provides visibility into on-chain activity. KYT applies that visibility within structured compliance workflows, connecting transaction data to risk scores, alert generation, investigation processes, and regulatory reporting obligations. Analytics is the data layer. KYT is thecompliance application of that data.

Can KYT monitor self-hosted wallets?

Yes. KYT solutions can assess transactions involving self-hosted wallets and identify relevant risk indicators including indirect exposure tohigh-risk services. This is particularly relevant under the Travel Rule, where interactions with self-hosted wallets may trigger enhanced due diligence requirements.

Does KYT support Travel Rule compliance?

KYT and Travel Rule compliance address different requirements but are complementary. KYT provides transaction-level risk context that supports the counterparty assessment required under the Travel Rule. Transaction data enriched by KYT helps organisations make informed decisions about whether to proceed with a transfer and whether enhanced due diligence isneeded.

How does KYT support SAR filing?

KYT generates structured alert outputs that document the specific risk indicators identified in a transaction or pattern of transactions. This documentation forms the evidentiary basis for a Suspicious Activity Report, providing the compliance team with the detail needed to complete a filing that satisfies regulatory expectations for specificity andcompleteness.

What should organisations look for in a KYT solution?

Key evaluation criteria include: blockchain network coverage (number and range of supported chains), entity database depth and recency, hop-depth analysis capability, alert quality and false positive management,investigation workflow features, scalability to transaction volume, jurisdiction-specific compliance support, and integration with existing KYC andcase management systems.

How often should monitoring rules be reviewed?

At minimum annually, and more frequently if transaction volumes grow significantly, new product lines are added, major enforcement actionshighlight new typologies, or significant changes occur in the regulatory frameworks applicable to the organisation. The review should be documented asevidence of a live compliance program.

Can KYT reduce false positives?

Well-designed programs reduce false positive rates through higher-quality entity attribution, more precise risk intelligence, and regularcalibration of detection thresholds to the actual risk profile of the business. Reducing false positives is as important as generating true positives: alert fatigue is a genuine compliance risk.

Is KYT relevant for stablecoins?

Yes. Stablecoins are subject to the same AML monitoring obligations as other crypto assets under MiCA, the FCA MLRs, FinCEN guidance,VARA rules, and MAS Notice PSN02. Monitoring stablecoin transactions requires aKYT solution that covers the range of stablecoins in circulation acrossmultiple chains.

What is hop depth and why does it matter?

Hop depth refers to the number of intermediate wallet transfers between a transaction and a high-risk entity. A transaction may be one hop fromyour direct counterparty, or it may be four hops away through intermediatewallets. Regulators including OFAC have taken action in cases involving indirect exposure, making hop-depth analysis an essential component ofsanctions screening and AML monitoring.

How does KYT differ from traditional transaction monitoring?

Traditional transaction monitoring operates within closed banking systems and focuses on account-level behavioural patterns. KYT extends monitoring to open blockchain networks, providing wallet attribution, hop-depthanalysis, cross-chain tracing, and entity-level risk scoring that legacysystems are not designed to perform.

How Scorechain supports KYT

An effective KYT program requires more than blockchain visibility. Organisations need the ability to understand risk in context, investigate alerts efficiently, demonstrate complianceoutcomes to regulators, and scale as transaction volumes grow.

Scorechain platform capabilities

• Monitor blockchain transactions across 50+ supported networks including Bitcoin, Ethereum, Solana, Avalanche, Polygon, and major layer-2 protocols

• Assess wallet and transaction risk with hop-depth exposure detection across 939,000+ labelledentities

• Screen 470+ stablecoins across supported chains as part of standard transaction monitoring

• Generate risk-scored alertswithin 300 milliseconds via API, enabling pre-settlement intervention

• Process 1.5 million+ AMLchecks daily at institutional scale

• Support investigation workflows with structured case files, entity attribution, and hop-depth pathvisualisation

• Generate audit-ready documentation capable of supporting regulatory examination and SAR filing

• Integrate with broader AML, KYC, Travel Rule, and casemanagement frameworks

scorechain.com | Enterprise blockchain analytics and cryptoAML compliance platform

scorechain.ai | On-demand wallet screening reports forcompliance teams

Headquartered in Luxembourg. Serving banks, CASPs, payment providers, custodians, and asset managers across the EU, UK, UAE,Singapore, and globally.

Final thoughts

The question facing banks, CASPs, Payment providers, and Asset managers is no longer whether to implement KYT, but whether the program they have is adequate for the regulatory environment they now operate in.

Across the EU, UK, US, UAE, Singapore, and every jurisdiction that has adopted FATF standards, the direction of regulatory travel is consistent: firms must demonstrate not justthat monitoring policies exist, but that controls are effective, calibrated,and generating defensible compliance decisions in practice. The era ofcompliance-by-documentation is ending. The era of compliance-by-evidence has arrived.

Know Your Transaction is how organisations produce that evidence. Done well, it transforms blockchainactivity into a documented audit trail that satisfies regulators, protects theinstitution, and enables confident participation in digital asset markets. Done poorly or not at all, it represents a regulatory exposure that enforcement actions in the US, Europe, and the Gulf have shown can be existential.

The firms that build rigorous KYT programs now are not just managing compliance obligations. They are buildingthe operational foundation for long-term, trusted participation in an assetclass that is becoming central to the global financial system.

Note: Regulatory frameworks are updated periodically. Organisations should verifycurrent requirements with qualified legal or compliance advisors in eachrelevant jurisdiction.